Indemnity health plans are a popular alternative insurance option heavily marketed to contingent workers. These plans can provide high commissions to the firms marketing them, and as a result, can be very profitable. Also, they are often loaded with hidden high fees and expenses that increase their overall costs.

One strategy to capture these profits for the benefit of your organization and workers is to establish a health insurance captive. This option is particularly suitable for commercial staffing firms with 15 or more internal employees, as well as many professional and skilled trades staffing firms. Compared to workers’ compensation captives, health insurance captives have minimal capital requirements and tail liabilities, making them easier to implement.

A health insurance captive is essentially a private insurance company that self-insures health insurance for the captive’s owners (employers). While only the largest employers truly self-insure, most employers who self-insure also purchase reinsurance or a “stop-loss” insurance policy that reimburses claim expenses above a set claim liability. A captive is a way to self-insure with this kind of reinsurance.

How does a captive work?

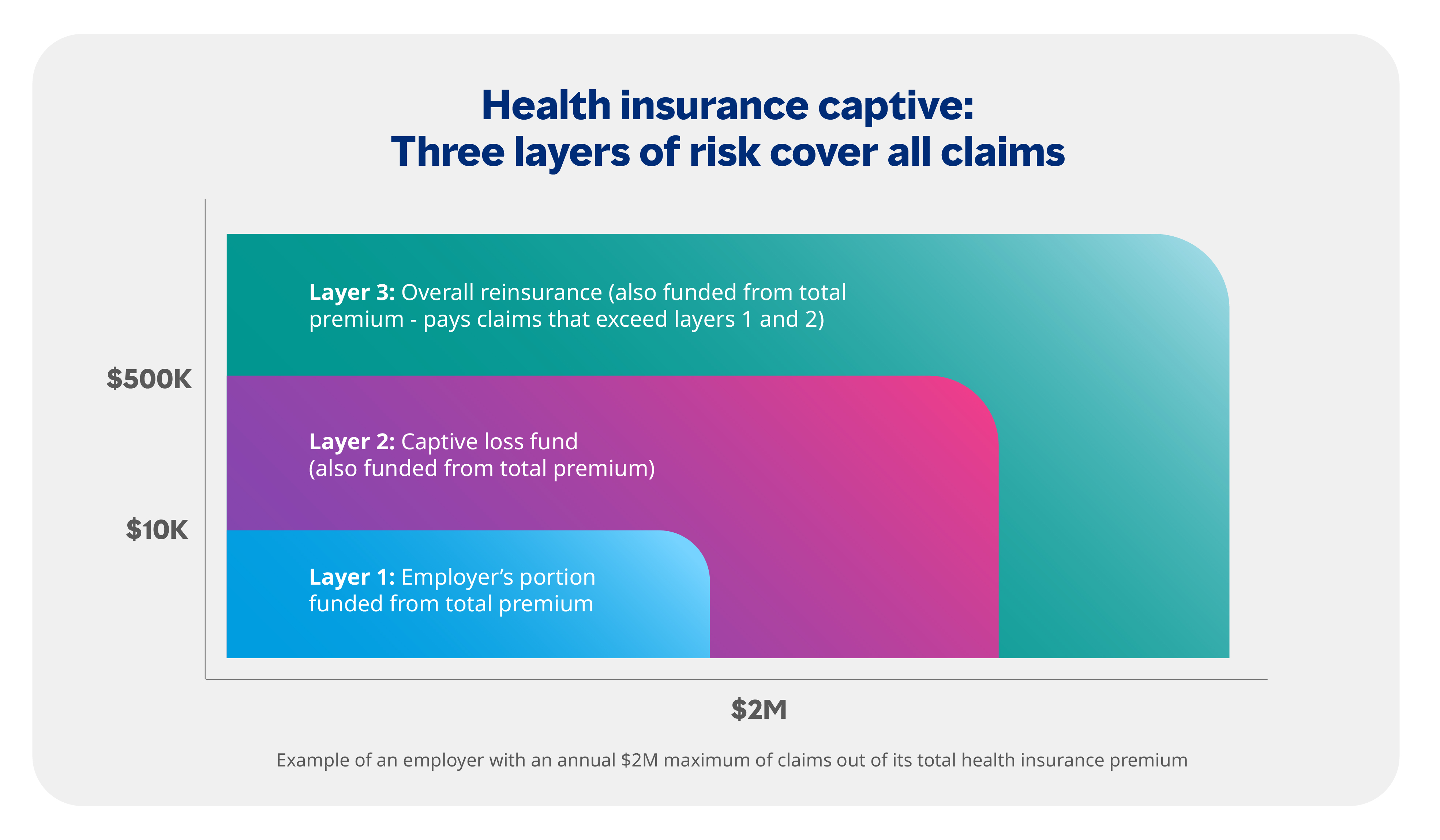

Typically, there are 3 layers of self-insurance and reinsurance:

Layer #1 is completely self-insured by the employer, capped at a specific dollar amount for total claims and within that total amount there is also a maximum number of claims for any one person, such as $10,000. For example, an employer might have an annual claims maximum of $100,000, but any one person’s claims would be capped (i.e. $10,000).

Layer #2 is a pool funded by part of the reinsurance premiums contributed by all employers in the captive. This bulk of reinsurance premiums go into this pool. This is the captive layer that covers claims that exceed the limits of layer #1, up to an actuarially defined maximum for all claims combined and for any one person’s claim up to a certain amount.

Layer #3 is provided by a commercial reinsurance company. This covers medical expenses that exceed the combined limits set in layers #1 and #2 are covered by the reinsurer with no annual or lifetime cap, ensuring the employer’s health plan is in compliance with the Affordable Care Act (ACA). Total cost for all three layers plus administration and other fees is about the cost of a fully insured health plan.

A captive can be structured as a group captive, where multiple employers, possibly all staffing firms, collaborate to form and operate a captive together, or as a single parent captive, where a single employer operates its own captive. This can be done within a larger captive model where the layers noted above still work to pool risk with other employers. A single parent captive can have the added advantage of creating an asset on the employer’s books using consolidated financial statements in accordance with GAPP (Generally Accepted Accounting Principles).

Advantages of captives

- Captives can significantly reduce healthcare expenses by:

- Capturing underwriting profits that would normally go to the insurer.

- Reducing or eliminating fees and expenses of fully insured plans.

- Combining all employee health insurance plans, allowing underwriting profits of one group of employees can be used to subsidize the expenses of other employees

- Reducing/controlling commissions and fees.

- Captives also provide greater control over health benefits and expenses by:

- Escaping or reducing the dependency on the traditional health insurance market

- Providing flexibility over plan design and choice of vendors (PPO networks, administrators, etc.).

- Generating investment income on claim reserves.

- Using greater risk management over healthcare expenses

- Transparency

- Captives can offer better health insurance by:

- Allowing each employer to benefit from the stability of a larger pool of employees.

- Leveraging buying power.

Whether or not you currently offer indemnity benefits to your temporary workers, a captive can be a beneficial financial model that enhances coverage for your internal employee’s better coverage while providing more stable and lower costs.

For more information on deciding whether a health insurance captive is right for your staffing firm, please contact a Marsh McLennan Agency (MMA) representative.