In the world of finance and risk management, surety bonds and letters of credit (LOCs) are two essential tools that serve to protect parties involved in contractual agreements. While both mechanisms provide a form of financial assurance relating to your performance obligations they operate differently and are suited for distinct purposes.

In the world of finance and risk management, surety bonds and letters of credit (LOCs) are two essential tools that serve to protect parties involved in contractual agreements. While both mechanisms provide a form of financial assurance relating to your performance obligations they operate differently and are suited for distinct purposes.

Similarities between surety bonds and letters of credit

At their core, both surety bonds and letters of credit are designed to mitigate risk and ensure that obligations are met. They act as guarantees that a party will fulfill their contractual duties, whether it’s completing a construction project or making a payment. In both cases, if the principal fails to meet their obligations, the beneficiary can claim compensation from the surety or the bank issuing the LOC.

Surety bonds

- Surety – the bond provider guaranteeing the principal’s performance

- Principal – the entity with an obligation to perform

- Obligee – the beneficiary of the bond

Letter of credit

- Issuing Bank – the financial institution that issues the letter of credit

- Applicant (Buyer) – the entity that requests the letter of credit

- Beneficiary (Seller) – the entity that receives payment

Key differences between surety bonds and letters of credit

The primary difference lies in the nature of the guarantee. A surety bond involves three parties: the principal (the party required to perform), the obligee (the party receiving the benefit), and the surety (the entity providing the bond). The surety assumes the risk and guarantees the performance of the principal. If the principal defaults, the surety is responsible for fulfilling the obligation, often through financial compensation.

In contrast, a letter of credit is a financial instrument issued by a bank on behalf of a client, guaranteeing payment to a third party, provided that certain conditions are met. The bank’s obligation is to pay the beneficiary upon presentation of specified documents, regardless of the underlying transaction’s performance.

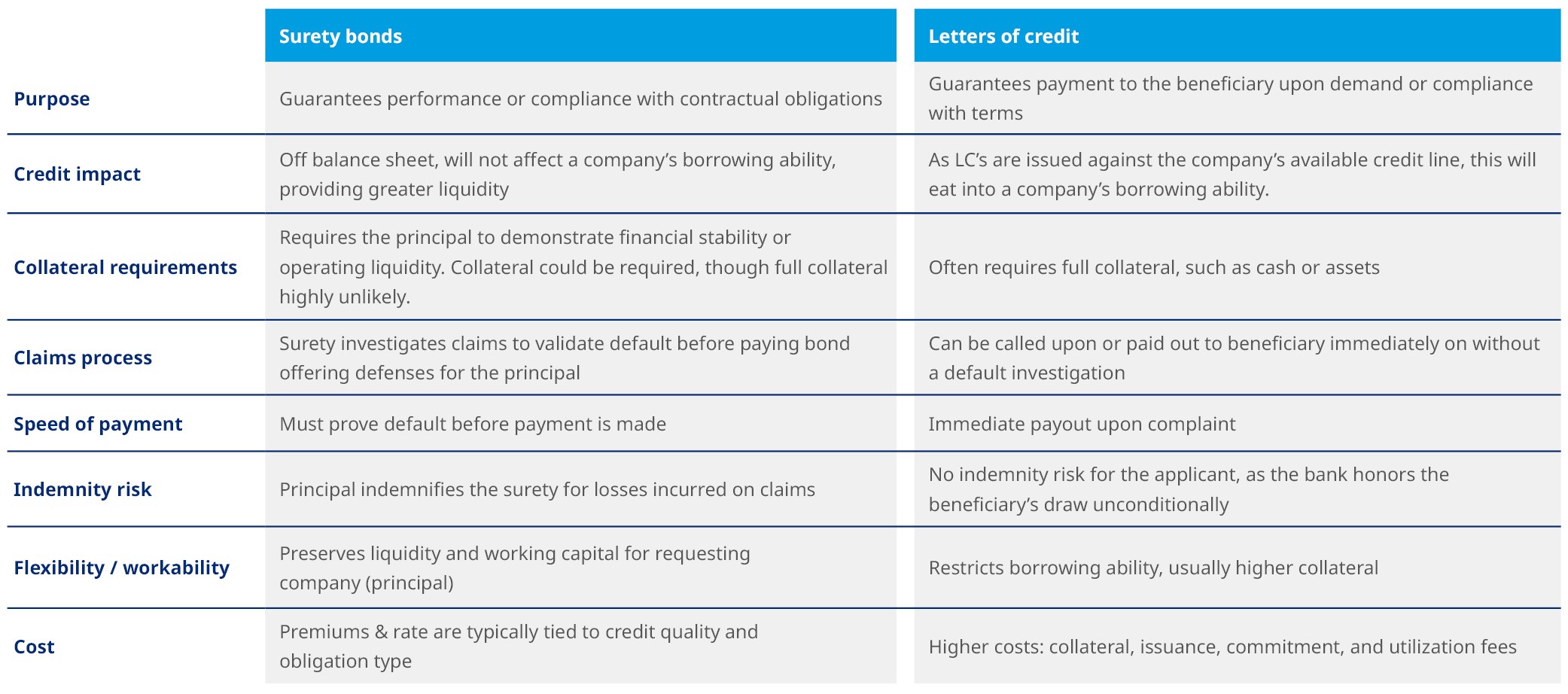

Here’s a comparison chart to help simplify it.

Why surety bonds are more beneficial

Surety bonds are often considered more beneficial for several reasons. First, they provide a stronger assurance of performance since the surety conducts thorough underwriting and risk assessment before issuing the bond. This process ensures that only financially stable and capable parties are bonded, reducing the risk of default.

Second, and this is a drastic difference between the two. A surety’s claims handling process is there to protect its principal in a claim situation & investigate validity of its claims. Whereas a LOC just pays out in any case without an investigation.

A surety bond is a financial tool. In many cases a bond can be used in lieu of either cash or letters of credit. Given its popularity and strong underwriting, bonds are growing in acceptance across several industries.

Additionally, surety bonds can enhance a contractor’s credibility and reputation, as they demonstrate financial responsibility and reliability. This can lead to more business opportunities and better terms in contracts.

What is a surety-backed letter of credit?

A surety-backed letter of credit combines the strengths of both instruments. In this arrangement the surety company provides a guarantee to the bank that issues the letter of credit. This arrangement enhances the creditworthiness of the LOC, as the surety company assumes some of the risk. It allows for greater flexibility in financing while still ensuring that obligations are met.

To learn how we can assist your business with surety needs, check out our surety practice.